India’s AI Gold Rush: How a $10 Billion Market is Reshaping the Global Tech Supply Chain

India’s artificial intelligence market is experiencing a transformation that rivals the country’s IT services boom of the early 2000s, but with one crucial difference: this time, India isn’t just providing the talent—it’s building the entire ecosystem from silicon to solutions.

The numbers tell a compelling story. India’s AI market is projected to reach $7.84 billion by 2025 and potentially $31.94 billion by 2031, representing a remarkable 30.6% CAGR. But behind these projections lies a more complex narrative about supply chains, infrastructure buildout, and strategic positioning that positions India not just as a consumer of AI technology, but as a critical node in the global AI infrastructure.

The Infrastructure Foundation: More Than Just Code

The most striking aspect of India’s AI evolution is its infrastructure-first approach. India currently operates 152 data centers with over 1,180 MW of IT load capacity, with an additional 45 new data centers planned for 2025 adding 1,015 MW of capacity. Mumbai alone accounts for 37 facilities, making it one of the world’s hottest data center construction markets.

This isn’t merely about building more server farms. The shift to AI workloads fundamentally changes infrastructure requirements. Copper emerges as a critical component, with hyperscale AI data centers consuming up to 50,000 tons of copper per facility compared to 5,000-15,000 tons for conventional data centers. This dramatic increase stems from the power density requirements of AI server racks and sophisticated cooling systems needed to prevent hardware failure.

The cooling challenge alone represents a market opportunity. The cooling systems market in India is projected to grow from USD 2.38 billion in 2025 to USD 7.68 billion by 2030, representing a 26.42% CAGR. Companies like Blue Star and Voltas are positioning themselves alongside global players like STULZ and Johnson Controls to capture this demand.

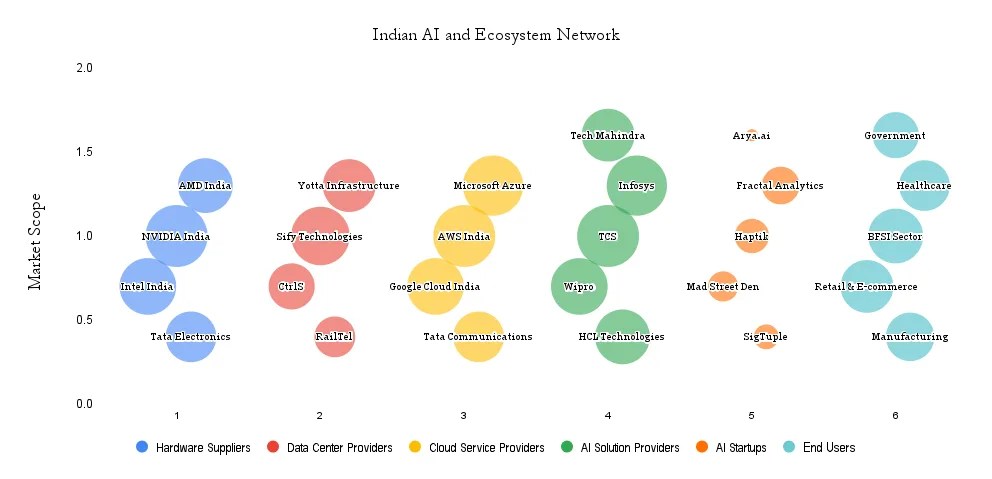

The Nine-Layer AI Supply Chain: India’s Strategic Positioning

What makes India’s AI story unique is how it’s developing capabilities across the entire technology stack. The AI ecosystem functions through eight to nine practical layers, each with different economics and risk profiles: from raw materials and semiconductors to applications and end-user services.

At the foundation, companies like STL, HFCL, Polycab, and KEI provide fiber and power cables, while Hindalco and Hindustan Copper supply essential metals. Moving up the stack, Tata-PSMC and CG Power-Renesas-Stars are developing fab capabilities, while Nxtra, STT, NTT, Yotta, CtrlS, Web Werks, and AdaniConneX operate data centers.

The semiconductor layer presents both opportunity and challenge. The government’s IndiaAI Mission employs a tender-based procurement approach for 10,000+ GPUs, representing an investment of approximately ₹4,000 crore, with individual high-end GPUs costing ₹20-40 lakh per unit. This creates opportunities for AMD and Intel to compete more effectively against NVIDIA’s current 80% market dominance.

The Talent Arbitrage Advantage

India hosts 16% of the global AI talent pool, with over 600,000 AI professionals currently employed and projections reaching 1.25 million by 2027. But the real advantage isn’t just in quantity—it’s in the ecosystem density. India hosts 520+ technology incubators and accelerators, ranking third globally in active programs, with 42% focused on AI and related technologies.

This concentration creates network effects. Companies like Fractal Analytics, which spun off Qure.ai for medical imaging, demonstrate how talent density enables rapid specialization and commercial spin-offs. The ecosystem has supported 2,000+ AI startups launched over the past three years, creating a virtuous cycle of expertise development and capital formation.

Sectoral Adoption: Where the Money Flows

The adoption pattern reveals India’s unique market dynamics. BFSI represents the most mature AI adoption segment, with 70% of companies maintaining well-defined AI strategies and 82% actively implementing proof-of-concepts. This isn’t surprising given the sector’s data richness and regulatory push for digital transformation.

Healthcare presents the highest growth potential. AI-led diagnostics make medical services viable in Tier 2 and rural regions, expanding addressable demand substantially. Companies like SigTuple, which develops computer vision for blood and urine analysis, and Qure.ai’s chest X-ray analysis demonstrate how AI can leapfrog traditional healthcare infrastructure limitations.

Manufacturing shows a different pattern. Companies like Tata Steel utilize AI for supplier performance monitoring and logistics optimization, while the broader sector integrates predictive maintenance and quality control systems. The sector transformation is quantifiable: digital technologies are expected to command 40% of total manufacturing expenditure by 2025, up from 20% in 2021.

The Government Catalyst: IndiaAI Mission’s Strategic Impact

The government’s IndiaAI initiative aims to create national AI compute infrastructure with access to over 10,000 graphics processing units (GPUs) for training and research, with ₹10,000 crore ($1.17 billion) corpus. This isn’t just funding—it’s strategic infrastructure development that democratizes access to computational resources.

The initiative’s structure reveals sophisticated thinking about AI ecosystem development. Rather than simply funding startups or research, it addresses the fundamental constraint: compute access. Latest rounds add ~3,850 accelerators and introduce Google Trillium TPUs alongside Nvidia H100s, creating competitive dynamics in hardware procurement while building national capabilities.

Risk Factors and Supply Chain Vulnerabilities

The infrastructure buildout faces real constraints. Power availability and grid upgrades, especially in metro hubs, cooling and water constraints for high-density AI halls, and semiconductor/accelerator allocation risks represent systemic challenges. Mumbai’s rise as a data center hub is creating grid strain that analysts are flagging as a potential bottleneck.

The semiconductor dependency remains acute. Despite domestic fab initiatives, India still relies heavily on imported GPUs and specialized AI chips. Tata Electronics’ ₹27,000 crore investment in Assam facility represents progress toward indigenous capabilities, but the timeline for meaningful domestic production extends beyond the current AI adoption wave.

The Global Context: India’s Positioning Strategy

GenAI alone could lift India’s GDP by $359–$438B by 2030 (5.9–7.2% of GDP), according to EY analysis. This isn’t just about domestic market capture—it’s about positioning in global AI value chains.

India’s approach differs markedly from China’s state-directed model or the US’s private sector-led development. The combination of government infrastructure investment, private sector innovation, and regulatory frameworks that encourage rather than constrain development creates a distinctive model. India’s scalable public digital infrastructure including Aadhaar, UPI, DigiLocker, and ONDC creates data-rich environments essential for AI model training.

Investment Implications: Where Capital is Flowing

The supply chain analysis reveals investment opportunities across multiple layers. Data center REITs and infrastructure funds are capturing the physical buildout demand. Specialized AI solution providers targeting specific verticals—healthcare diagnostics, financial risk assessment, supply chain optimization—demonstrate stronger unit economics than horizontal platform plays.

The talent arbitrage remains compelling, but the value is shifting toward companies that can combine Indian engineering capabilities with domain expertise and global market access. Companies like Mad Street Den (Vue.ai) offering visual recognition solutions for fashion retailers, or Locus providing AI-powered supply chain optimization, demonstrate how specialized knowledge creates sustainable competitive advantages.

Looking Forward: The 2027 Inflection Point

NASSCOM-BCG projects $17B by 2027 at 25-35% CAGR, with spending ramp largely in services plus pilots scaling in FY26-27. This timeline suggests we’re currently in the infrastructure buildout phase, with commercial deployment scaling significantly over the next 2-3 years.

The critical success factors are becoming clear: local manufacturing capabilities, talent development aligned with industry needs, government policy alignment, deep sector specialization, and ecosystem integration across supply chain layers. Companies demonstrating these capabilities are positioning for disproportionate value capture as the market scales.

India’s AI transformation represents more than market growth—it’s the emergence of a new model for technology ecosystem development that combines state infrastructure investment with private innovation and global integration. The $25-30 billion market projection by 2030 may prove conservative if execution continues at the current pace.

The question isn’t whether India will become an AI powerhouse, but how quickly it can build the complete stack from silicon to solutions while maintaining the openness and innovation culture that makes its tech sector globally competitive.